In the finance world, pre-approval is a very important first step before you do big transactions like getting loans or making purchases. It means that a lender has looked at how good your credit is and decided if they will give you money to borrow - also known as "approve" - and for what amount plus interest rate in return for paying back the loan over the period agreed upon with them. This article will explain pre-approval deeply, talking about what it means, why it matters so much in finance dealings, and how one gets this kind of approval along with its many kinds.

Definition of Pre-Approval

Pre-approval, the crucial first step in many financial dealings, tells people who want to borrow money how much they can borrow. It is different from pre-qualification because it gives a more accurate estimate. Pre-approval happens when lenders do a thorough evaluation of your financial past such as credit score and history, income details like salary or earnings from business ventures along with assets you possess, and any debts owed to others. Lenders use these factors to decide the highest amount a borrower can borrow and also establish terms for the loan. Knowing this information gives power to the borrowers, helping them make wise decisions about their financial promises.

Additionally, pre-approval is like a precursor that makes the transaction process run more smoothly. When borrowers have a letter of pre-approval, they become more believable to sellers or lenders because it shows their seriousness and ability to handle financial matters. This can be especially useful in markets where there is strong competition among buyers as sellers might give preference to those who are already pre-approved. Moreover, pre-approval helps in preventing disappointments as it gives borrowers a clear understanding of their ability to borrow. This stops them from overcommitting financially.

- Documentation Accuracy: Ensure all documentation provided for pre-approval is accurate and up-to-date to avoid delays or discrepancies during the evaluation process.

- Credit Score Impact: Understand that multiple pre-approval inquiries within a short period can temporarily lower your credit score, so it's essential to limit applications to necessary transactions only.

Significance of Pre-Approval

The significance of pre-approval extends beyond mere formality; it serves as a strategic tool for both buyers and lenders. For homebuyers, pre-approval offers a competitive edge in real estate transactions. In a seller's market, where demand outweighs supply, sellers are often inundated with multiple offers. A pre-approved buyer stands out among the competition, as their financial readiness reassures sellers of a smooth and timely transaction. This can result in preferential treatment, potentially leading to better negotiating power or even a lower purchase price.

Additionally, pre-approval speeds up the loan application procedure which is a win-win situation for borrowers and lenders. When a thorough evaluation is done beforehand, lenders can quickly notice any possible problems or differences, allowing them to deal with these concerns in advance. This more efficient method reduces the time and resources needed for final approval, helping borrowers to get their funding faster. Moreover, before approving can assist borrowers in comprehending their monetary restrictions. This will guide them to make knowledgeable choices about their borrowing requirements.

- Market Dynamics Awareness: Stay informed about market conditions, as pre-approval can be especially advantageous in competitive real estate markets where multiple offers are common.

- Financial Preparedness: Use pre-approval as an opportunity to reassess your financial situation and determine a comfortable borrowing range based on your current income, expenses, and financial goals.

How Pre-Approval Works?

The process of obtaining pre-approval involves several steps, each designed to assess the borrower's creditworthiness and determine the terms of the loan. It begins with the borrower applying to a lender, typically online or in person. Along with the application, borrowers are required to provide supporting documentation, such as pay stubs, tax returns, bank statements, and authorization for a credit check. These documents offer insights into the borrower's financial stability, income sources, and existing debts.

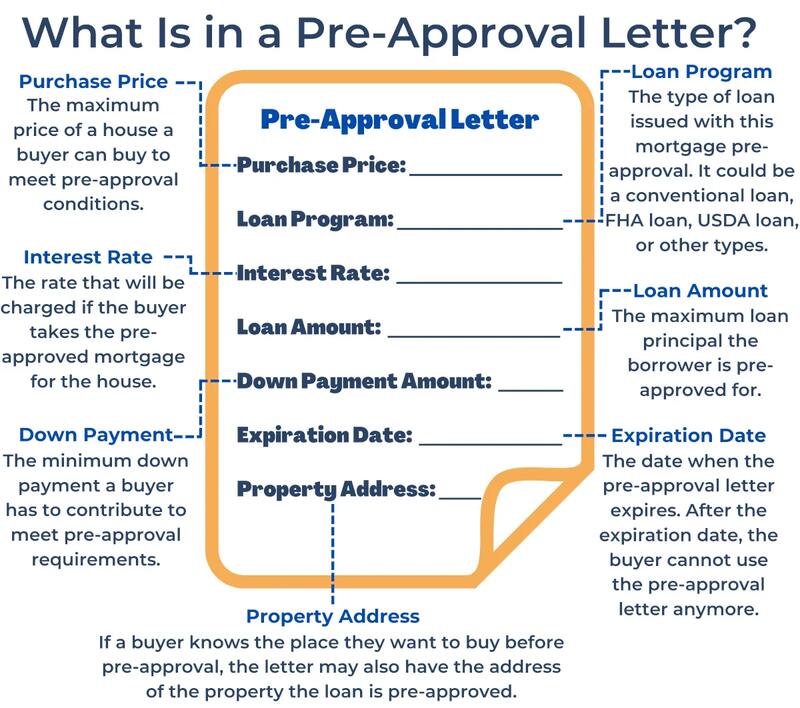

When the lender gets the application along with documents, they will do a deep examination of the borrower's financial picture. They first check if all details given are correct and then look at things like credit score, how steady income is, work history as well as a ratio between debts and income. After this assessment is done, it helps in deciding what could be the highest amount of loan and interest rate that fits for borrower. When the borrower fulfills the criteria of the lender, they are given a pre-approval letter that talks about all aspects and rules related to getting this loan.

- Document Organization: Keep all financial documents organized and readily accessible to streamline the pre-approval process and ensure timely submission of required information.

- Communication with Lender: Maintain open communication with your lender throughout the pre-approval process to address any questions or concerns promptly.

Types of Pre-Approval

Different financial needs and goals are met by different kinds of pre-approval, giving those who borrow money more options and ease in getting financing. Among the most usual forms is mortgage pre-approval, especially in real estate. People who plan to buy a home get mortgage pre-approval so they can calculate how much they can borrow before starting their search for houses. This helps them to limit their search to houses that fit in with their budget and make a believable offer to sellers, which speeds up the buying process.

A different kind of pre-approval that is quite common, especially for people planning to purchase a car, is known as auto loan pre-approval. When you get pre-approved for an auto loan, it makes buying a car easier because first, before going to any dealership - you already know how much money you can spend and what your various financing choices are. This gives buyers the power to bargain from strength and sidestep the pushiness often associated with in-house financing offers at dealerships. Another beneficial aspect is that before receiving credit cards or personal loans, it enables borrowers to know their eligibility and conditions. This assists them in making choices about their borrowing requirements with all the necessary information at hand.

- Loan Comparison: Compare pre-approval offers from multiple lenders to identify the most favorable terms and conditions for your financial situation.

- Pre-Approval Validity: Be aware that pre-approval letters typically have an expiration date, so it's essential to act promptly to capitalize on the terms offered.

Conclusion

To sum up, the pre-approval is significant in many financial dealings. It helps borrowers know how much they can borrow and it also makes applying for a loan easier. People who go through pre-approval show themselves as serious buyers or borrowers, which improves their possibility of getting what they want while not wasting time on things that might not work out. Knowing the meaning, importance, steps, and kinds of pre-approval allows people to make knowledgeable monetary choices and handle the intricacies of borrowing with self-assurance.